The “Unstoppables” – RBC Wealth Management

By Frédérique Carrier and Jim Allworth

-

AI spending by both tech and non-tech companies will continue to grow, in

our view, driven by the unacceptably high cost of being left behind. -

The cost of caring for and financing individuals who are no longer earning

income will escalate as the world’s population ages. -

Renewables will become the dominant source of power, in our opinion, as

they have become the cheapest sources of energy. -

After rapid expansion and falling costs, utility-scale storage facilities

are a game changer for ensuring reliable energy infrastructure.

Unremitting AI spending

Spending on the development and application of artificial intelligence (AI)

will accelerate further from today’s already lofty levels as tech

companies—from “mega” to “mini”—struggle to avoid being left irretrievably

behind. The annual spending on AI by Microsoft alone has tripled since 2020 to

reach close to $60 billion.

At the same time, non-tech businesses are ramping up investment in AI

applications to keep their cost structures competitive. To illustrate, the AI

bookings of Accenture, a global professional services company, reached over $2

billion in the first three quarters of fiscal 2024 (ending August), compared

to a much more muted $300 million in all of fiscal 2023.

So far, there has been little to no financial return on these investments, but

most companies committed to this spending argue that there is already a high

”experiential” return which may prove vital in a business striving to remain

competitive in the future. The possibility of being left behind makes

under-spending a risky strategy, in our view. The U.S. Census Bureau estimates

that only 6.6 percent of American companies use AI for business purposes, a

share which is likely to continue to grow going forward, in our opinion.

AI equipment manufacturers and software providers have been the clear

beneficiaries of the new technology, with their stock valuations having

expanded markedly. We think investment portfolios would likely benefit from

exposure to the infrastructure beneficiaries of generative AI (GenAI)—e.g.,

electricity production, transmission, and storage, as well as data

centre/server farm construction, and data transmission—where the eventual

spending may take a decade or more to arrive.

Shares of companies which adopt the new technology solutions may also benefit,

but we believe investors should assess how the new technology is being

implemented—to increase sales, reduce costs, or improve productivity—and keep

an eye on the competition. If competitors are also using GenAI effectively,

any competitive advantage may erode quickly.

For more on this theme, please see these articles from our “Innovations”

series:

The gray wave

A growing elderly population around the world will have to be cared for. We’ve

been watching the inevitable approach of a massive “gray wave” for a couple of

decades—now it’s here. In all the major economies (and most of the rest) the

proportion of the population over the age of 65 is already surging to levels

never seen before. Even the over-80s cohort, once an insignificant minority,

is rapidly becoming a component to be reckoned with everywhere. The global

population of people 65 years and older will approach 1.6 billion by 2050,

according to the UN.

The cost of caring for a fast-growing segment that is no longer earning income

is a problem desperately looking for a solution(s). The Alzheimer’s

Association estimates that in 2024, total U.S. health care costs for all

individuals 65 years and over suffering from Alzheimer’s disease reached $360

billion, or as much as cancer and cardiology care combined. It also points out

that millions of family members and unpaid caregivers provided 18.4 billion

hours of care, valued at $346.6 billion in 2023.

Given these onerous costs borne by both governments and households and that up

to 20 percent of life is spent battling chronic diseases in later years,

scientists are focusing on lengthening healthspans, or the number of years a

person is healthy in old age.

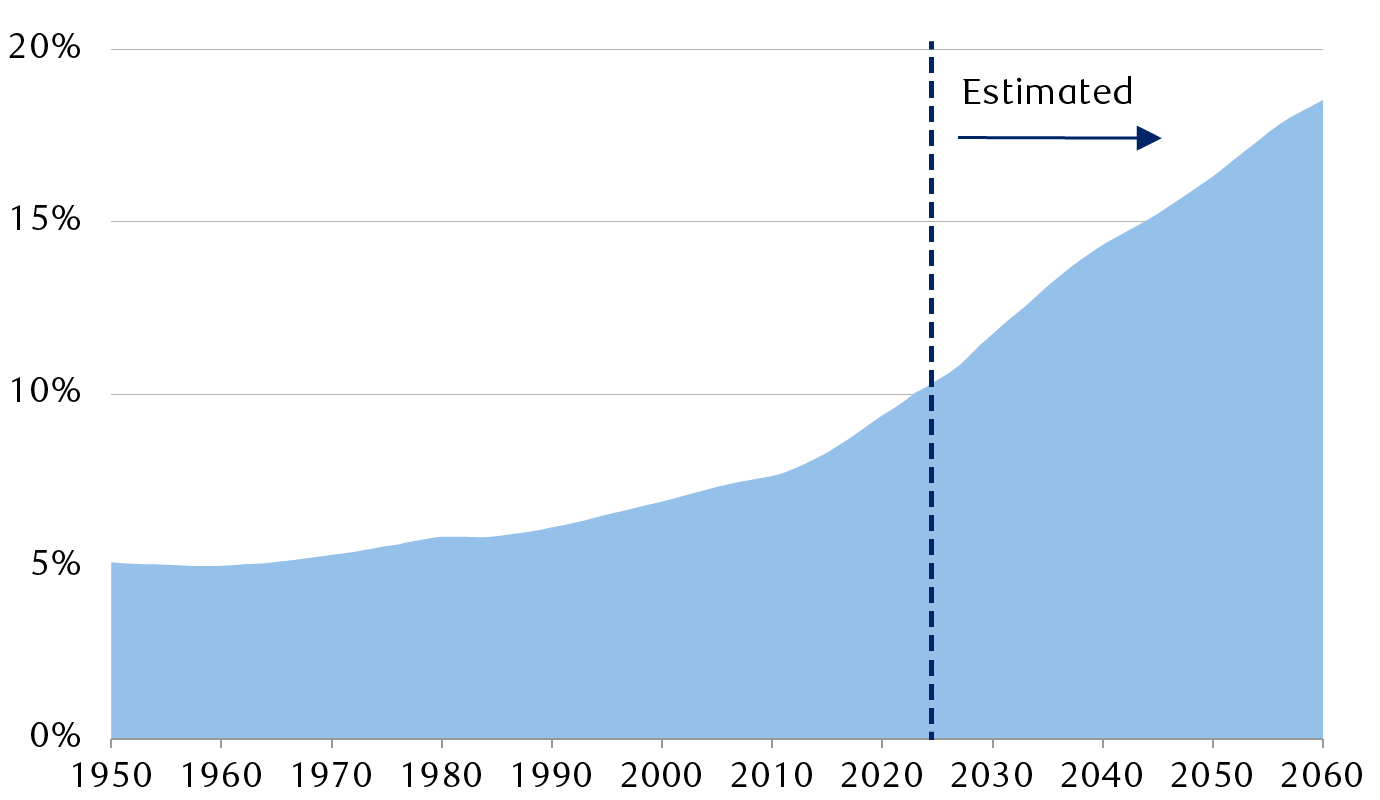

Percentage of world population over the age of 65

The line chart shows the percentage of individuals aged 65 and over in the

world population. In 1950, people over 65 represented roughly five percent

of the total population. By 2024, that proportion had doubled. The UN

estimates that by 2060, nearly 20% of the world population will be aged 65

and over.

Source – United Nations World Population Prospects 2024

Ideas on how to implement this theme into investment portfolios include:

-

Biotech companies that prioritize diseases with a meaningful unmet need and

demonstrate that they are able to execute on well-designed clinical trials -

The financials industry (e.g., wealth management and insurance) as

individuals will need to consider how not to outlive their savings -

Homebuilders looking to meet increased demand to accommodate both

multi-generational households and single-occupancy homes

The unabating march of renewables

Renewables are set to become the dominant source of power, in our view.

Kick-started by government subsidies more than two decades ago, the rapid

installation of wind farms, solar collectors, and now energy storage

facilities have driven the cost of renewable power (without subsidies) down to

levels that could soon make it the lowest-cost energy source in many

countries. In fact, costs per kilowatt hour from renewables have plummeted to

a degree not imagined two decades ago.

As a result, close to a quarter of U.S. electricity now derives from

renewables, close to one-third in China, and an even higher 46 percent in the

UK, as of 2023, according to Our World in Data.

Solar and onshore wind projects break even at the lowest electricity prices

Global levelized cost of electricity, USD/megawatt-hour (MWh)

The chart shows the long-term breakeven price a power project needs to

recoup all costs and meet the required rate of return for different

electricity sources: solar, wind (offshore and onshore), combined cycle

gas turbine, and coal. Solar and onshore wind now enjoy the lowest

breakeven prices.

-

Combined cycle gas turbine

-

Coal

-

Wind (onshore)

-

Wind (offshore)

-

Solar

The levelized cost of electricity (LCOE) is the long-term break-even price

a power project needs to recoup all costs and meet the required rate of

return. The levelized cost does not include subsidies or tax credits. Data

for coal and gas power plants not available prior to 2014.

Source – BloombergNEF

Despite the incoming Trump administration prioritizing U.S. fossil fuel

production, the adoption of renewables will almost certainly continue, in our

view, thanks to striking cost advantages.

Texas, which has long been the U.S. state synonymous with fossil fuels, is now

the nation’s leader in wind energy, while having also tripled solar energy

production in the last three years, according to the Texas Comptroller of

Public Accounts.

Texas is not alone in capitalizing on renewables’ cost advantage. For more

than a decade, global installation of new solar power generation has routinely

exceeded the International Energy Agency’s (IEA) five-year forecasts,

sometimes by 100 percent or more.

The Global Solar Council estimates that global installed solar capacity has

reached two terawatts—that is, two trillion watts or the equivalent of some

seven billion solar panels installed—enough to power one billion homes. That

is double the installed capacity reached only two years ago, an astonishing

rate of growth.

Permitting for new renewable projects has proven to be a bigger time hurdle

than construction of the projects themselves. The permit approval backlog is

high and growing, suggesting that the growth of new renewable power

installations is not likely to slow appreciably anytime soon.

Investable ideas include renewable energy equipment manufacturers and

providers of energy storage, energy efficiency, and/or smart grid solutions.

The electrification of everything

Lower costs for renewable energy, with the promise of more installed capacity

to come, are a harbinger that more energy will be used, even more so as the

intermittent nature of wind and solar is addressed.

Technical, managerial, and systems-engineering improvements have been changing

the design and management of traditional power grids to accommodate renewable

sources. As a result, at certain times, more than 95 percent of California’s

power can be generated by wind and solar, while Denmark can run its entire

grid solely on wind.

But the rapid expansion of utility-scale storage facilities, the so-called

grid-scale batteries, is the real game changer, in our view. Traditionally,

hydroelectric power acted as large-scale storage, moving water between

reservoirs at the top and bottom of a hill. Although dependent on topography,

there are a great many sites worldwide that are physically and politically

feasible for development of pumped hydro storage—enough to meet double the

current electricity consumption, according to estimates from an Australian

National University study. However, the recent surge in interest rates and

construction costs has probably made many of those sites less financially

viable than utility-scale storage facilities.

Today, giant batteries arranged in rows of sheds are the preferred technique

to store power. These installations are finally taking off as prices are

falling. BloombergNEF, a research group, estimates that the average price of

stationary lithium batteries per kilowatt-hour of storage fell by some 40

percent in the five years to 2023. Meanwhile, new technologies and chemistries

are also being developed. Promising alternatives include sodium-ion and

nickel-hydrogen batteries.

The IEA believes that 90 gigawatts of battery storage was installed globally

in 2023, or twice the amount installed the previous year. Bain & Company,

a consultancy, estimates that the market for grid-scale storage could expand

by at least 40 percent annually to the end of the decade, and possibly beyond.

Energy is a major input cost for many industries, businesses, and households.

Getting plentiful, low-cost renewable energy to where it is needed from where

it is produced is a major industrial enterprise on its own.

From the rapid increase in the number of server farms necessitated by AI and

the proliferation of data centres, to energy-intensive industries like steel,

cement, and chemical production, to the increased worldwide need for air

conditioning as global temperatures rise, we believe electricity demand looks

likely to go on rising sharply even as the cost of renewable power is falling.

Grid-scale batteries can enhance energy resilience, balancing fluctuations in

supply and demand. In our opinion, those countries which combine grid-scale

batteries with nuclear energy, such as China and France, can create

particularly robust and reliable energy infrastructure. Investment

opportunities abound, in our view.

Plugging portfolios into the future

The “Unstoppables”—the four key themes we’ve described—are long-term secular

trends which will likely play out over the next decades. We believe that

portfolios should be able to benefit from exposure to these growth areas.

However, investors will also need to ensure that the macroeconomic environment

is favorable, business models are sound, and share valuations are not too

widely out of sync with growth prospects, no matter how alluring they may be.

For more on the equity outlook for 2025, please see our other 2025 Outlook

focus article, Equity balancing act.

View the full Global Insight 2025 Outlook here

RBC Wealth Management is a business segment of Royal Bank of Canada. Please click the “Legal” link at the bottom of this page for further information on the entities that are member companies of RBC Wealth Management. The content in this publication is provided for general information only and is not intended to provide any advice or endorse/recommend the content contained in the publication.

® / ™ Trademark(s) of Royal Bank of Canada. Used under licence. © Royal Bank of Canada 2024. All rights reserved.

link