It’s been a privilege – RBC Wealth Management

April 8, 2025

Atul Bhatia

Fixed Income Portfolio Strategist

Portfolio Advisory Group–U.S.

Key points

-

The dollar’s reserve status may not be as important to the U.S.

economy as is often assumed. -

Issuers of reserve currencies face fiscal and trade headwinds that are

problematic for the U.S. -

We think reserve holders are likely to slowly diversify into other

currencies, helping reduce the risks of the transition.

“An exorbitant privilege” is how former French President Valéry Giscard

d’Estaing once referred to the U.S. government’s ability to issue the

global reserve currency.

And there’s no question—in our minds—that the dollar’s role as the world’s

savings vehicle contributed to U.S. economic success in the last 75 years.

But currency leadership has less helpful consequences as well, including

fiscal and trade imbalances. With the dollar’s role in the global economy

evolving—and in our view likely declining—we think this is an opportune

moment for investors to consider what comes next and how changing currency

appetites are likely to impact the global economy.

Contrary to popular wisdom, we believe there’s a strong case to be made

that the exorbitant privilege of reserve status is now a net liability for

the U.S. and that a shift to a more balanced global currency reserve

basket is likely a more stable framework for global economic activity. At

the same time, a potential declining role for the dollar represents the

weakening of another global unifying force, with likely negative

implications for U.S. leadership and possibly global political stability.

The good

Currency reserves are simply an economist’s way of describing how a nation

chooses to store its savings. Countries save for many reasons, but their

primary goal is to secure access to food, fuel, and other critical inputs

in the event of a domestic economic crisis. Countries could choose to save

these materials directly—like the U.S. does with its strategic petroleum

reserve—but that requires significant storage and defense costs. Most

countries instead hold a basket of foreign currencies, relying on their

ability to trade those holdings for needed goods and services. Since World

War II, the majority of world savings has been held in U.S. dollars; the

greenback’s current share of global saving is roughly 60 percent.

This reliance on the U.S. currency for savings has two main implications.

First, countries that hold dollars want to make sure that trade continues

to be denominated in dollars. They’ve bought into the ecosystem, and if

trade starts shifting over to rubles or euros or yuan, then their dollar

savings may not be helpful in a crisis. A country could try to switch to a

different currency, but that’s an expensive—and risky—move: make the wrong

choice or move too soon and your country could be locked out of vital

markets. It’s much easier to perpetuate the current system and support the

dollar as the trade vehicle.

For the U.S., having the dominant currency involved in global trade

matters. The theoretical benefit is that it eliminates the risk that the

U.S. cannot buy needed inputs. That’s nice, but given the size of the U.S.

economy, not a lot of folks were losing sleep over that risk. The real

benefit of the dollar’s role in trade, in our view, is that small and

midsize U.S. companies have a much easier time expanding into export

markets. Hedging currency risk is complicated and often involves a

tradeoff between protecting margin and satisfying customers. A U.S.-based

exporter selling in dollars avoids those costs and headaches, making it

easier for firms to begin exporting earlier in their corporate

development.

The other main benefit to having the reserve currency is that it helps

keep government borrowing costs down. Once foreigners have acquired

dollars, they need a low-risk, easily accessible way to hold them, and

that tends to mean owning U.S. Treasury bonds. This demand for government

securities has helped reduce long-term borrowing costs, giving a financial

boost to the U.S.

Not all sunshine

But not all the consequences of being the source of the world’s reserve

currency are positive.

To begin with, there’s the basic issue of how foreigners can acquire

dollars. There are only three ways:

- They can be given them, through financial aid;

-

They can borrow them, typically by having central banks exchange blocks

of their respective currency in a so-called “currency swap” arrangement; - Or they can earn dollars through a trade surplus.

Since countries tend to grow their reserves over time, the U.S.

effectively needs to run a persistent trade deficit if it wants the dollar

to retain its share of reserves. The only alternative means of providing

dollars to foreign savers is through large amounts of financial aid,

potentially to strategic rivals, or by having the U.S. Federal Reserve run

an extremely complicated and potentially risky book of multicurrency swap

lines globally. Both alternatives are political and economic nonstarters,

in our view, so the U.S. can choose between a trade deficit or a

diminishing percentage of global reserves in the long run. It’s not a

coincidence that the U.S. has run trade deficits for decades.

Once foreigners have acquired dollars, they need a place to store them,

and that usually means Treasury bonds. The flipside of being the reserve

currency and borrowing cheaply is that a country must issue enough debt to

keep up with reserve holder demand. A key reason why countries have shied

away from euro reserves, in our view, is the lack of truly eurozone-wide

debt and the insufficiency of German and other perceived low-risk

sovereign bonds. The recent push by Germany to expand issuance to fund

defense spending could help increase the attractiveness of the euro as a

reserve currency, in our view.

Certainly, U.S. fiscal deficits go well beyond what is required for

foreign reserve growth, but even if the U.S. federal government shifted

toward a more balanced budget, a persistent budget surplus is problematic

for a reserve currency issuer.

Too expensive?

When the U.S. began running persistent fiscal deficits in the 1980s, the

stock of federal debt outstanding was around 30 percent of GDP. Today,

existing debt is closer to 120 percent of GDP. The numbers for trade are

directionally similar, although to a lesser degree.

Separating out the impact of currency reserve status on debt accumulation

and trade levels is beyond art versus science. There are simply too many

variables moving simultaneously to reach robust conclusions.

We think it’s fair to say, however, that a reasonable person could

conclude that the marginal cost of additional debt accumulation is higher

at 120 percent of GDP than 30 percent of GDP, and that expanding U.S.

trade deficits from their current levels will likely exacerbate domestic

economic and political concerns. In short, the longer the U.S. runs these

imbalances, the greater the costs become.

The benefits of reserve currency status, arguably, have not kept pace.

What comes next?

So far, we’ve been discussing the dollar’s reserve currency role and its

implications for the U.S., but the issue is, of course, global in nature.

For nations accumulating reserves, we see a real possibility that tariffs

and their impact on international trade prove to be the driver for

rethinking reserve strategy.

As we’ve discussed elsewhere, we think the Trump administration’s tariff

policies are designed to exploit foreign nations’ reliance on American

consumption. It’s an incredibly powerful lever, in our view, for the U.S.,

and by extension it’s a key strategic liability for both allies and

rivals. While the Trump tariffs are the most immediate and explicit

reminder of other countries’ economic dependence on the U.S., there’s a

long history of Washington using unilateral economic sanctions and

freezing dollar assets. This has generated significant international

pushback and resentment, primarily from organizations like the BRICS, a

multilateral group founded by Brazil, Russia, India, China, and South

Africa.

Given the U.S.’s increasing willingness to flex its economic might, we

would be surprised if countries did not seek to better balance their own

internal supply and demand, reducing reliance on the U.S. consumer. The

shift away from international trade is likely to lead to slower global

growth as the efficiencies from trade are lost. This is a dynamic that has

been going on for years, as we’ve previously discussed in our “Worlds apart” series, but we believe tariff threats are likely to accelerate the

shift.

Countries tend to base their reserve balances on the value of their

imports, so if countries shift away from trade and toward more of a

balanced domestic economy, they will likely find themselves with excess

reserves.

Our expectation is that most countries would maintain current reserve

levels. This would essentially allow them to “grow into” their current

stock of savings versus aggressively drawing down reserve totals to match

a reduced import bill. The reason for our view is simple—drawing down

reserves is a risky move, and central bankers by their nature tend to be

risk averse.

Emerging currencies fill the space created by the U.S. dollar’s declining

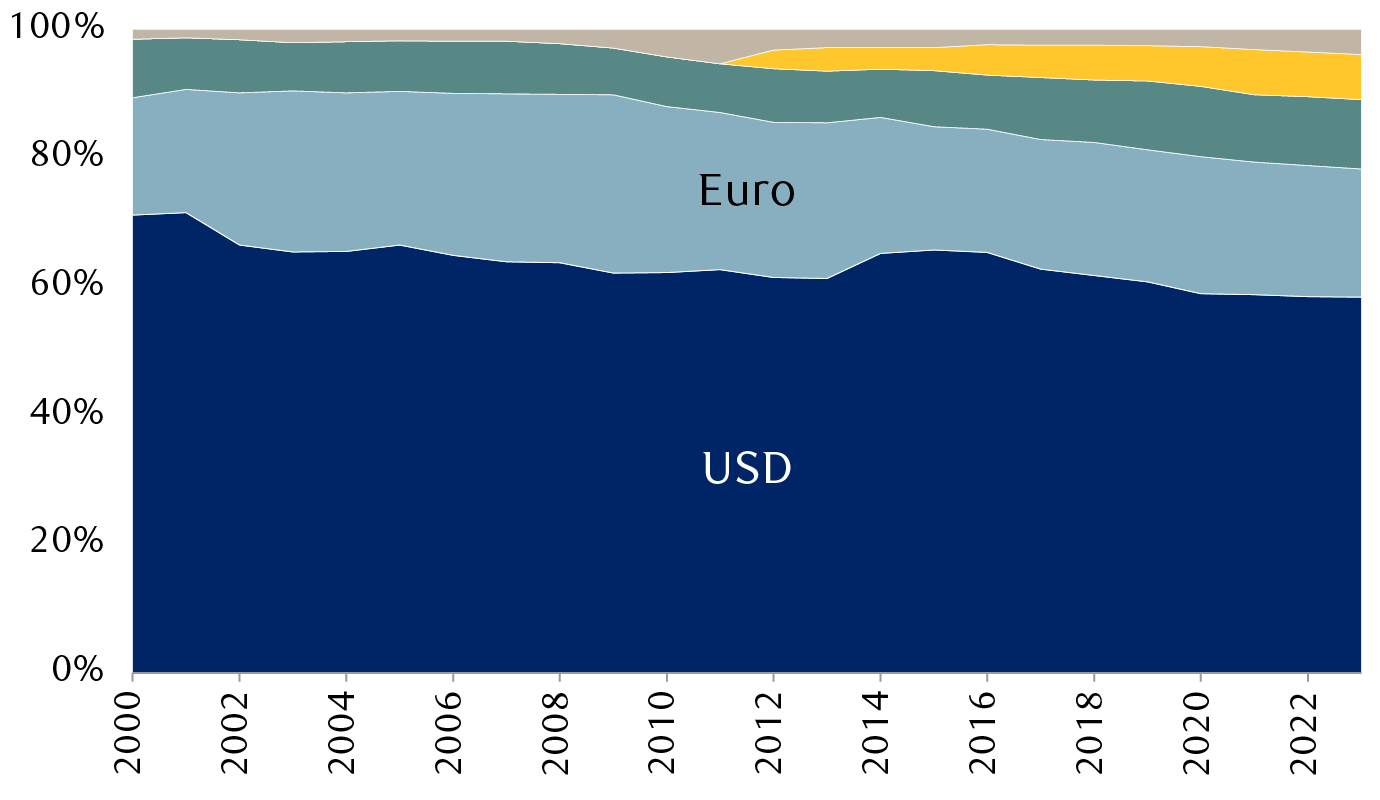

role in global reserves

Share of global currency reserves

The chart shows the percentage of global reserves held in various

currencies: the U.S. dollar; the euro; other traditional reserve

currencies (Japanese yen, British pound, Swiss franc); and major

non-traditional reserve currencies (Chinese renminbi, Canadian dollar,

Australian dollar). The percentage of reserves held in U.S. dollars

fell to roughly 58% in 2023 from roughly 71% in 2000. Approximately

half of the dollar’s decline was offset by increases in the major

non-traditional reserve currencies, which were not significant before

the early 2010s and now account for roughly seven percent of global

reserves.

-

Other

-

Major non-traditional (CAD, AUD, RMB)

-

Other traditional (JPY, GBP, CHF)

Source – RBC Wealth Management, International Monetary Fund

Once nations re-enter a phase of reserve accumulation, we would expect

them to add to their savings with a focus on non-dollar currencies. This

is exactly the behavior we’ve seen since the turn of the century.

The risk that a country would move to immediately shift its currency

composition—essentially sell Treasuries and dollars and buy euros or

yen—is mainly theoretical. No other currency offers sufficient high

quality, stable value, liquid investment alternatives to act as a dollar

replacement. Unless or until that changes, the practical choice, in our

view, is dollar savings or lower savings.

If this interpretation proves correct, the short-term outcome is nearly

ideal for the U.S. Investing nations would continue to roll over their

Treasury holdings and dollar-based international trade would remain the

norm. Some degree of regional trade would likely migrate to a different

currency, but if most countries continue to hold Treasuries, the incentive

to trade in U.S. dollars remains.

Longer term, the U.S. would no longer enjoy its exorbitant privileges, but

it would also not face the inherent need to provide both dollars and debt

to the world. Less helpfully, a world that is less dependent on the U.S.

consumer is also less invested in the health of the U.S. economy.

Historically, foreign nations have not had much reason to push hard during

economic negotiations with the U.S.; after all, for most of the world a

healthy U.S. economy was key for their domestic economies’ production and

profits. From our vantage point, if and when countries shift toward

regional trade partners and their own domestic buyers, all sorts of

bilateral discussions look less cooperative and more like a zero-sum game.

Bretton Woods, Bancor, and beyond

The idea that the existence of a single reserve currency can create global

imbalances is nothing new. John Maynard Keynes is perhaps best known for

his statement that “in the long run, we’re all dead,” but he also was one

of the first to identify the inherent instability of a single currency

acting as the global reserve. He made a push at the Bretton Woods

Conference in the 1940s to base international trade on a global unit of

account called the Bancor, rather than the U.S. dollar.

The idea was to have all trade settled in Bancors and run through an

international clearing union. Countries that ran either a Bancor surplus

or a deficit would be charged a penalty rate on the imbalance. This would

provide incentives for trade to remain largely balanced. The idea has been

refloated on occasion, most notably following the global financial crisis,

but it has failed to be adopted largely because, in our view, countries

have been unwilling to cede that degree of control to an international

body. While we think the idea of a global unit of account has significant

merit, we see the geopolitical barriers as nearly insurmountable.

Instead of a radical transformation, we believe currency reserves are

likely to go through an evolutionary process. Falling trade will lead to

slower global growth and declining reserve needs, but the reduction will

likely be done passively. Some countries may choose to rebalance part of

their holdings away from the dollar, but the lack of “safe” investment

options for non-dollar currencies will act as a constraint, in our

opinion.

While any shift away from dollar reserves is likely to be presented as a

negative for the U.S. economy, we are not convinced the facts support that

interpretation. Instead, we think we’ve reached the point Keynes foresaw,

where the fiscal and trade implications of issuing the reserve currency

outweigh the rather limited benefits of reserve status.

In other words, we believe that in the long run Keynes may be dead, but

he’s still got a point.

RBC Wealth Management, a division of RBC Capital Markets, LLC, registered investment adviser and Member NYSE/FINRA/SIPC.

Fixed Income Portfolio Strategist

Portfolio Advisory Group–U.S.

link