June 18, 2025

Thomas Garretson, CFA

Senior Portfolio Strategist

Fixed Income Strategies

Portfolio Advisory Group – U.S.

Key points:

-

Though most central banks continued to lower short-term rates over the

first half of the year, longer-term sovereign bond yields defied rate

cuts to move higher. -

While there are numerous reasons long-term bond yields are shifting

higher, sovereign debt levels and risks, particularly in the U.S., the

UK, and Japan, are increasingly becoming drivers. -

Though a risk, we continue to believe deteriorating economic

fundamentals will be the primary driver of yields, which will see them

fade modestly in the second half of the year.

If volatility was the main market narrative of the first half of the year,

we expect the second half’s to be, well, more volatility.

Global bond markets have had to contend with issues on numerous fronts,

and on all sides. Issues such as tariff-related inflationary risks have

argued for higher yields, where the potential for tariff-induced slower

economic growth would argue for lower yields.

Though the trade war seems to have somewhat dissipated into the background

for now, tariffs remain both highly uncertain and likely to have ripple

effects into the second half of the year. And as is often the case, one

source of volatility is more likely than not to simply be replaced by

another. The next risk for global bond markets may come from inside the

building—sovereign bonds.

Lower interest rates, higher yields

The first chart below points to budding risks around government finances. While

most major central banks—save for Japan—have been slicing short-term

interest rates, longer-term sovereign bond yields have not only failed to

follow, they have moved in the opposite direction entirely.

For example, since the Federal Reserve delivered the first of a series of

rate cuts in September 2024, which ultimately amounted to 100 basis

points, longer-term Treasury yields have risen by an equal amount; a

similar story has played out in the UK.

While the rise in Japanese long-term yields may not be as surprising given

modest rate hikes from the Bank of Japan (BoJ), much of the recent spike

came on the back of unexpectedly weak investor demand at bond auctions in

May. Investors seem to have stayed away amid rising concerns about Japan’s

worsening fiscal trajectory.

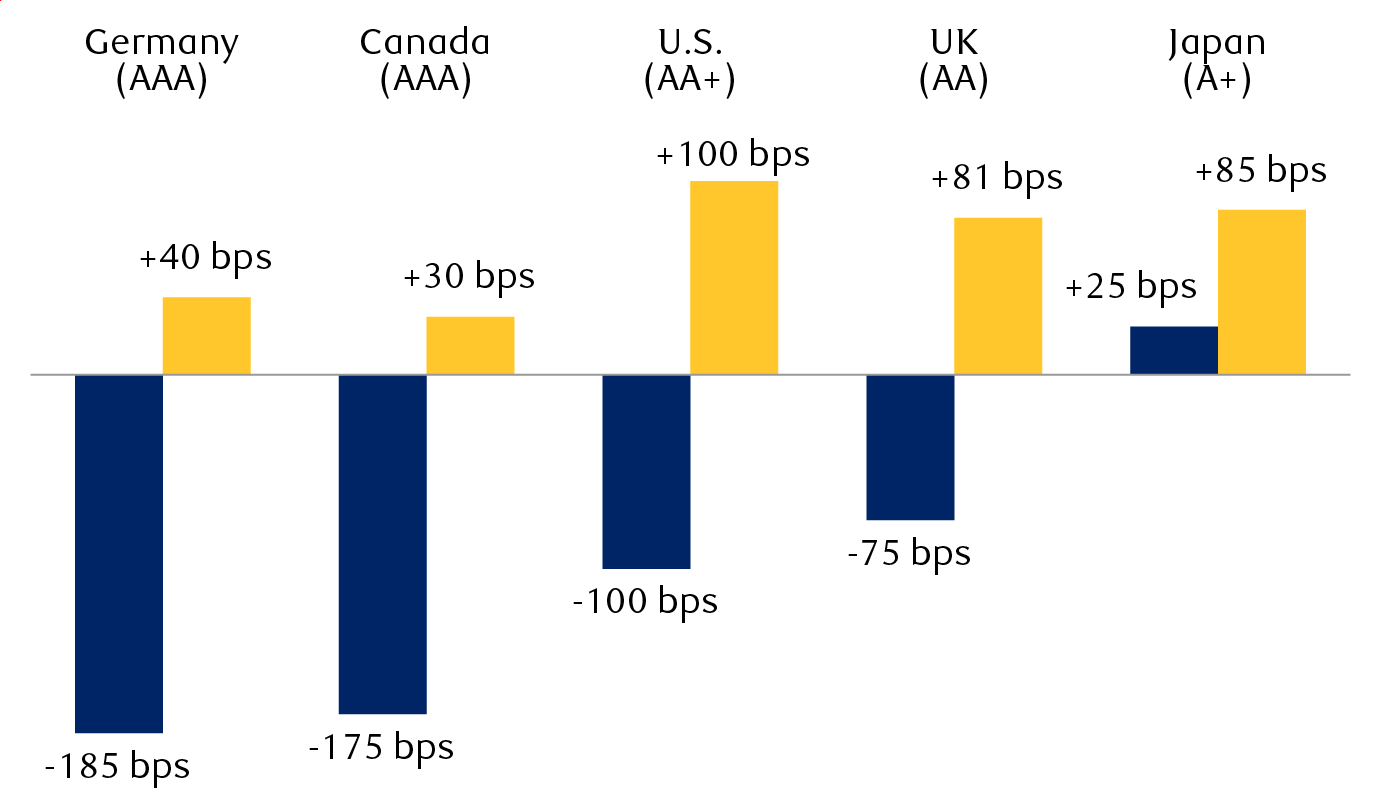

Despite central bank rate cuts, bond yields keep rising

The chart shows the change in central bank policy interest rates and

30-year bond yields since September 2024, and the aggregate credit

ratings from major rating agencies, for Germany (AAA rating; policy

rate -185 bps; yield +30 bps), Canada (AAA rating; policy rate -175

bps; bond yield +30 bps), the U.S. (AA+ rating; policy rate -100 bps;

bond yield +100 bps), the UK (AA rating; policy rate -75 bps; bond

yield +81 bps), and Japan (A+ rating; policy rate +25 bps; bond yield

+85 bps).

-

Change in central bank policy rates

-

Change in 30-year sovereign bond yields

Source – RBC Wealth Management, Bloomberg; shows net change from

9/1/24 through 5/30/25; composite credit ratings from major rating

agencies; Germany used as proxy for European Union; European Central

Bank rate cuts shown

Fiscal focus

And therein lies what could be the next source of market volatility this

year—sovereign credit fears.

Though long-term bond yields have also risen in Germany and Canada despite

even deeper rate cuts from both the European Central Bank and the Bank of

Canada, the more modest move higher may simply reflect fewer credit

concerns.

Following Moody’s downgrade of the U.S. credit rating in May, the U.S. now

holds an average credit rating of AA+, the UK is rated AA, and Japan is

A+. What about Canada and Germany? Both are still rated AAA with few

looming concerns on the fiscal front, in our opinion.

The UK has battled its own budget concerns in recent years as bond markets

most notably pushed back forcibly on previous tax cut and deficit

expansion plans in 2022. In the first quarter of this year, UK government

financing needs hit one of the highest levels on record as the yield on

30-year Gilts breached 5.6 percent, the highest level since 1998.

Then there’s the United States. While fiscal deterioration is nothing

new—and reasonably well-weathered by markets for decades—things risk

coming to a head later this year.

One factor in Moody’s decision was the expectation that the “One Big

Beautiful Bill Act” would add $4 trillion to the deficit over the next 10

years and that annual deficits would rise to around 9 percent, and that’s

assuming steady economic growth and full employment. Slower growth and/or

an outright economic downturn would likely only increase the deficit.

Though the final form of the bill remains to be seen, and the bias appears

toward being less of a deficit buster in the Senate, we think U.S.

deficits will almost certainly continue to trend in the wrong direction.

That will keep the focus on government bond auctions, and how governments

plan to finance themselves. After May’s spike in yields, the BoJ has

seemingly been able to calm markets by floating the idea of reducing long

bond issuance levels if demand is lacking. In the U.S., the Department of

the Treasury could also go down that path should there be signs that

domestic and foreign interest is lacking. That could serve to help keep

long-term yields lower, but there are also risks of shorter-term issuance

and refinancing risks, not to mention that the department may already be

overly reliant on short-term financing. There may be only bad, and not as

bad options, and that could be a lingering source of volatility itself.

Economic knock-ons

Finally, market optimism might be getting ahead of itself. Global risk

assets have seemingly been buoyed by central bank easing, but it may only

be phantom easing.

For example, when the Fed started cutting short-term rates last September,

the benchmark 10-year Treasury yield was 3.6 percent and the average 30-year

mortgage rate was 6.6 percent; at the end of May, those two metrics were higher

at 4.4 percent and 7.0 percent, respectively.

Despite the attempts of the Fed and other central banks to deliver

policy-easing measures, those efforts may not have had the desired impact.

The weight of higher sovereign bond yields—which tend to have a lagged

impact—could still pose a risk to economic activity globally through the

end of the year.

Risks, but paid for the risks

Global bond yields appear stuck between the threat of persistent inflation

and higher debt levels on the upside, and slowing economic growth and

rising unemployment on the downside.

The simple assumption would be that yields remain rangebound the rest of

the year. That said, we think that a slowing growth backdrop will

eventually prevail as the dominant driver of yields, and that global

yields will generally trend modestly lower into the end of the year.

And if there’s an upside to swelling sovereign balance sheets, it’s that

fixed income investors now have more options, and more yield. The

post-global financial crisis era of subdued government spending, sluggish

growth, and non-existent yield levels looks increasingly likely to be

relegated to the history books. Despite risks, at least investors are now

being compensated for those risks.

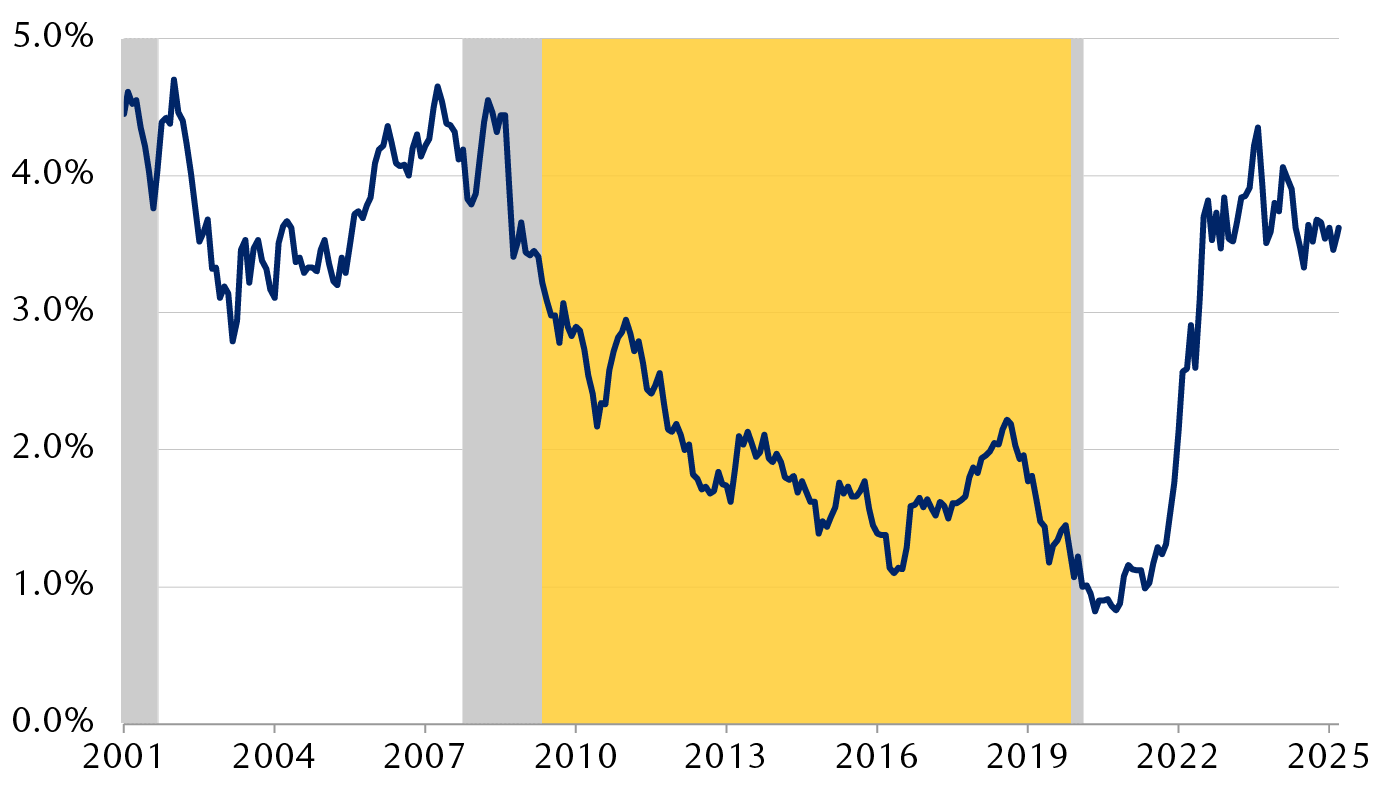

The era of low rates has been left behind

Bloomberg Global Aggregate Bond Index yield

The chart shows the average yield on the Bloomberg Global Aggregate

Bond Index since 2001. After falling sharply after the global

financial crisis in 2008, it has risen since 2021 to levels above

3.0 percent that were normal prior to that episode.

-

Recession

-

Post Global Financial Crisis

Source – RBC Wealth Management, Bloomberg

RBC Wealth Management is a business segment of Royal Bank of Canada. Please click the “Legal” link at the bottom of this page for further information on the entities that are member companies of RBC Wealth Management. The content in this publication is provided for general information only and is not intended to provide any advice or endorse/recommend the content contained in the publication.

® / ™ Trademark(s) of Royal Bank of Canada. Used under licence. © Royal Bank of Canada 2025. All rights reserved.

Senior Portfolio Strategist

Fixed Income Strategies

Portfolio Advisory Group – U.S.

link